Financial Information as of 31 March 2026

21 May 2026

Generali continues to deliver strong growth, supported by all segments. Solid capital position confirmed

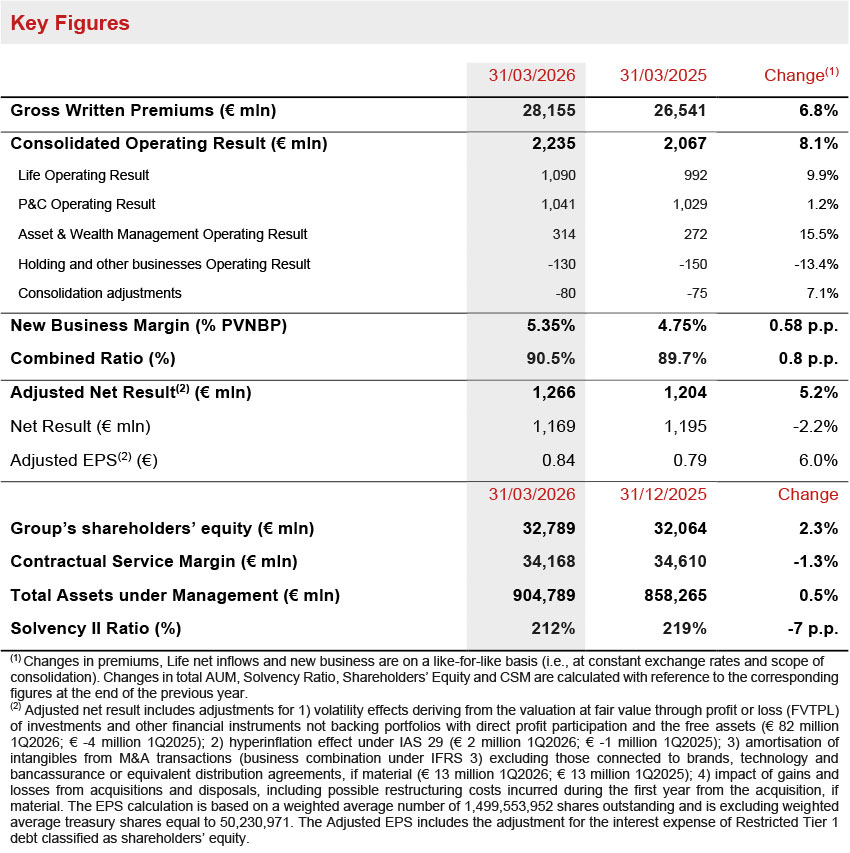

- Gross written premiums reached € 28.2 billion (+6.8%) driven by both Life (+7.5%) and P&C (+5.8%)

- Continued positive Life net inflows at € 4.3 billion, thanks to all business lines. New Business Value grew substantially to € 977 million (+19.1%)

- Combined Ratio at 90.5% (+0.8 p.p.) and undiscounted Combined Ratio at 93.1% (+1.1 p.p.) both impacted by Nat Cat events

- Asset & Wealth Management increased strongly (+15.5%) thanks to both Asset Management and Banca Generali

- Operating result grew significantly to € 2.2 billion (+8.1%), with positive contribution from all segments

- Adjusted net result increased to € 1.3 billion (+5.2% or +9.3% excluding a one-off tax component1). Adjusted EPS rose to € 0.84 (+6.0% or +10.2% excluding the same one-off tax component)

- Solid capital position with Solvency Ratio at 212% (219% FY2025)

Generali Group CFO, Cristiano Borean, said: “The Group’s first quarter 2026 results confirm the successful execution of our ‘Lifetime Partner 27: Driving Excellence’ strategic plan, with strong growth in the operating result supported by all segments, reflected as well in the adjusted net result. Life recorded a very strong business performance, thanks to the positive contribution from all business lines. In P&C, despite a higher impact from Nat Cat events, underlying technical profitability continued to improve. Asset & Wealth Management operating result benefitted from the strong performance of Generali Investments Holding and Banca Generali. Building on our strong balance sheet and high-quality diversified sources of cash generation, as well as a solid capital position, we remain fully focused on creating sustainable value for all our stakeholders.”

Executive summary

Milan – At a meeting chaired by Andrea Sironi, the Generali Board of Directors approved the Financial Information of the Generali Group at March 31st 20262.

Gross written premiums rose to € 28.2 billion (+6.8%), thanks to both Life and P&C.

Life net inflows were strong at € 4.3 billion, driven by all business lines.

The operating result grew to € 2,235 million (+8.1%), thanks to the positive performance of all segments.

The Life operating result increased to € 1,090 million (+9.9%) and the New Business Value improved to € 977 million (+19.1%).

P&C operating result grew to € 1,041 million (+1.2%) with the Combined Ratio at 90.5% (+0.8 p.p.) and the undiscounted Combined Ratio at 93.1% (+1.1 p.p.), reflecting a significant impact from Nat Cat events.

The operating result of Asset & Wealth Management reached € 314 million (+15.5%) driven by both the Asset Management result, which increased to € 142 million (+12.7%), and the Wealth Management result, which increased to € 172 million (+17.9%).

The operating result of the Holding and other businesses improved to € -130 million (€ -150 million 1Q2025).

The adjusted net result3 rose by 5.2% to € 1,266 million (€ 1,204 million 1Q2025). This reflected a tax amount of € 623 million, including a one-off component of around € 50 million in France, which increased the 1Q2026 tax rate by around 2.5 percentage points. Without this one-off tax item, the Adjusted Net Result growth rate would have been +9.3% and the Adjusted EPS growth would have been +10.2%.

The net result amounted to € 1,169 million (€ 1,195 million 1Q2025) reflecting the impact from financial markets on investments held at fair value through profit or loss during the first quarter as well as the aforementioned tax effect.

The Group’s shareholders’ equity increased to € 32.8 billion (+2.3%).

The Contractual Service Margin (CSM) decreased by 1.3% to € 34.2 billion (€ 34.6 billion FY2025).

The Group’s Total Assets Under Management (AUM) grew to € 905 billion (+0.5% compared to FY2025) with third party AUM accounting for € 387 billion, of which € 277 billion is managed by Asset Management.

The Group confirmed its solid capital position with the Solvency Ratio at 212% (219% FY2025), resulting from € 51.0 billion of Eligible Own Funds and € 24.1 billion of Solvency Capital Requirement.

The change primarily reflects the effect of market variances and the end of the grandfathering period, coupled with capital movements. These factors were only partially offset by the sound contribution from normalised capital generation supported by all business segments, despite higher Nat Cat. The normalised capital generation also included the full impact of the share buy-back for the Long-Term Incentive Plan (LTIP) executed in the first quarter.

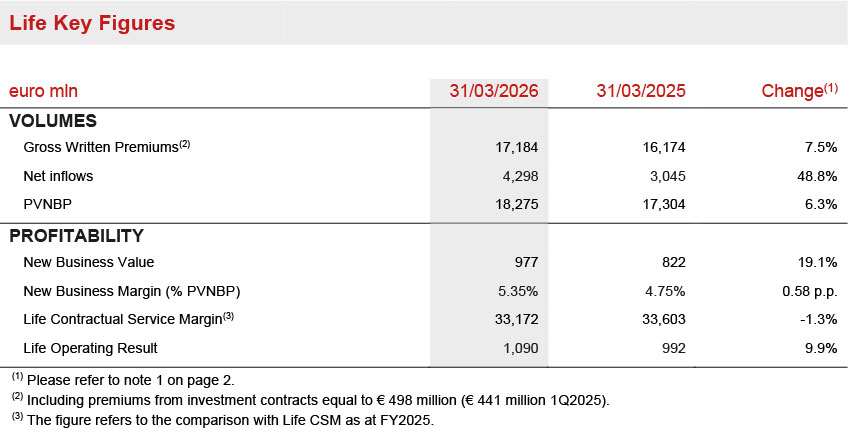

Life Segment

- Operating result rose to € 1,090 million (+9.9%)

- Life net inflows were very positive at € 4.3 billion, supported by all business lines

- New Business Margin was 5.35% (+0.58 p.p.); New Business Value (NBV) grew to € 977 million (+19.1%)

Gross written premiums in Life increased to € 17.2 billion (+7.5%) driven by traditional saving. Specifically, traditional saving recorded a strong increase (+21.8%), especially driven by Asia. Protection & health (+2.6%) grew in most countries in which the Group operates. Hybrid and unit-linked grew by 1.5%, with particularly strong performance in France.

Life Net inflows continued their strong upward trend, reaching € 4,298 million (€ 3,045 million 1Q2025), thanks to the positive contribution of all business segments. Traditional saving grew strongly by around 1.1 billion thanks to robust collection in Asia. Hybrid & unit-linked (+10.9%) grew mainly thanks to France. Protection & health products recorded a 1.9% increase, particularly in Italy, CEE and Spain.

New Business Volumes (expressed in terms of present value of new business premiums - PVNBP) rose to € 18.3 billion (+6.3%), mainly thanks to the solid hybrid & unit-linked production in France and traditional saving in Asia. New Business Value (NBV) grew significantly to € 977 million (+19.1%), supported by higher volumes and improved profitability. New Business Margin (NBM) increased to 5.35% (+0.58 p.p.) mainly thanks to the positive impact of a more favorable product mix and features as well as higher interest rates.

The Life Contractual Service Margin (Life CSM) stood at € 33,172 million (€ 33,603 million FY2025). The combination of New Business CSM of € 922 million and of the expected return of € 380 million more than offset the release of Life CSM for € 828 million.

The Life operating result increased to € 1,090 million (€ 992 million 1Q2025), driven by the improved operating insurance service result, which amounted to € 897 million (€ 816 million 1Q2025). The Operating Investment Result increased to € 193 million (€ 176 million 1Q2025).

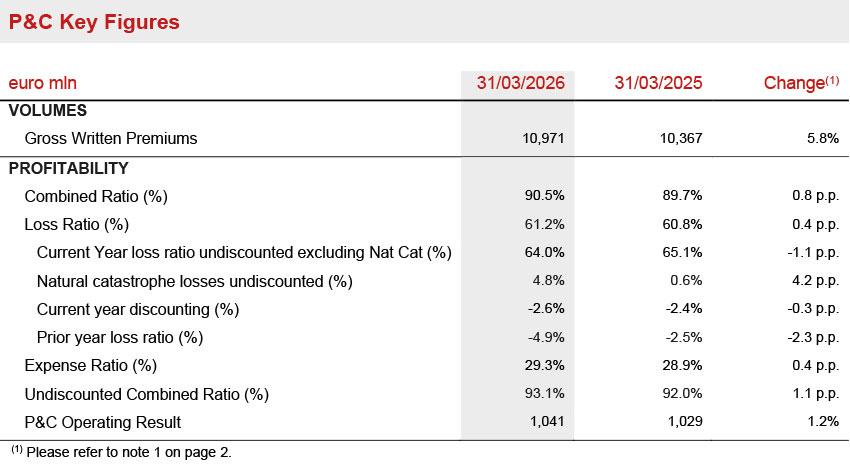

P&C Segment

- Premiums increased to € 11 billion (+5.8%)

- Operating result grew to € 1,041 million (+1.2%)

- Combined Ratio at 90.5% (+0.8 p.p.) and Undiscounted Combined Ratio at 93.1% (+1.1 p.p.) both reflecting higher Nat Cat losses

P&C gross written premiums grew to € 11 billion (+5.8%) thanks to the performance of both business lines. Non-motor was up 5.0% while motor rose by 6.0%. The growth was recorded across all main areas in which the Group operates. Considering also the accepted business underwritten by Europ Assistance, non-motor premiums grew by 5.3%. Excluding the contribution from Argentina, motor premiums increased by 4.5%.

The Combined Ratio increased to 90.5% (89.7% 1Q2025), reflecting undiscounted Nat Cat losses of 4.8 p.p., corresponding to € 426 million (0.6 p.p. 1Q2025, corresponding to € 48 million) in particular due to a very significant event in Portugal. This was partially offset by prior year development of 4.9 p.p. (2.5 p.p. 1Q2025). The current year attritional loss ratio (excluding Nat Cat) recorded a strong improvement, moving to 64.0% (65.1% 1Q2025). Current year discounting was equal to -2.6% (-0.3 p.p.). The expense ratio increased to 29.3% (+0.4 p.p.) driven primarily by higher acquisition costs, while the administrative component improved by 50 basis points year-on-year.

The Undiscounted combined ratio was 93.1% (92.0% 1Q2025).

The P&C operating result increased to € 1,041 million (€ 1,029 million 1Q2025). The operating insurance service result was € 854 million. The undiscounted current year operating insurance service result excluding Nat Cat increased by € 105 million compared to 1Q2025, marking a 21% year-on-year improvement. Current year discounting increased to € 235 million (€ 198 million 1Q2025). This result was achieved despite € 64 million of large man-made claims (€ 35 million 1Q2025).

The operating investment result improved by € 24 million to € 188 million thanks to higher investment income of € 371 million (€ 351 million in 1Q2025). The Insurance Finance expenses improved by € 4 million to € 184 million, driven by better unwinding of the Liability for Incurred Claims at € 142 million.

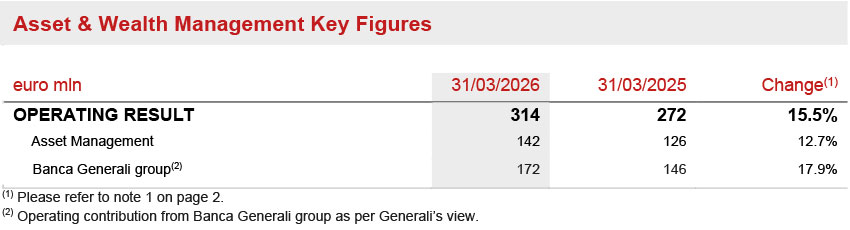

Asset & Wealth Management

- Asset & Wealth Management operating result rose to € 314 million (+15.5%)

- Banca Generali group operating result increased to € 172 million (+17.9%)

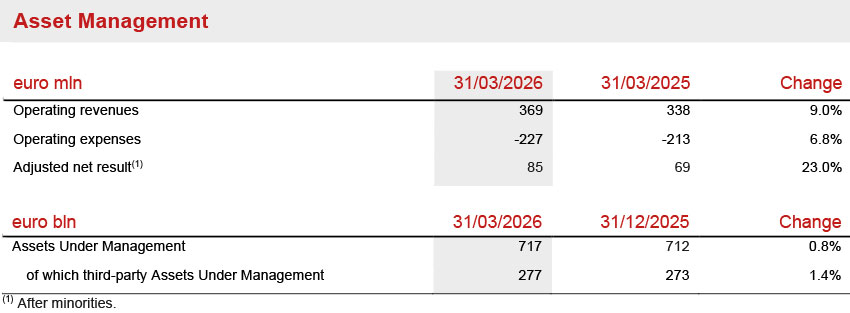

The Asset Management operating result increased to € 142 million (+12.7% compared to 1Q2025), mainly driven by higher recurring fees, reflecting higher average AUM. The contribution from non-recurring fees was € 15 million (€ 9 million in 1Q2025), stemming from higher transaction fees, reflecting a healthy deployment activity in the infrastructure business. Performance fees were € 2 million, in line with 1Q2025.

The operating result of the Banca Generali group grew to € 172 million (+17.9%) reflecting quality, diversification and strong operating trends coupled with higher performance fees. Total net inflows at Banca Generali in the period were € 1.9 billion.

Operating revenues rose to € 369 million (+9.0% vs 1Q2025), also benefiting from the consolidation of MGG Investment Group. Operating expenses increased to € 227 million (+6.8% vs 1Q2025), mainly due to the inclusion of MGG Investment Group and higher personnel costs.

The adjusted net result of Asset Management increased to € 85 million (+23.0%), also thanks to lower non-operating expenses compared to 1Q2025.

AUM pertaining to the Asset Management companies reached € 717 billion as of March 2026 (+0.8% vs FY2025), with the negative market effect offset by positive FX impact and net flows.

Third party AUM managed by the Asset Management companies grew to € 277 billion (+1.4% vs FY2025), supported by positive impact from FX rates movements and € 1.4 billion of positive net inflows during 1Q2026.

Holding and other businesses Segment

- Operating result at € -130 million

Operating result of the Holding and other businesses segment was € -130 million (€ -150 million 1Q2025).

The operating result of Other businesses was € 39 million (€ 12 million 1Q2025), with the prior year impacted by a one-off exit tax payment related to the closure of a foreign entity. Holding operating expenses increased by 4.5%, also due to costs related to share-based payments.

Outlook

The global macroeconomic environment continues to be affected by the uncertain outcome of ongoing negotiations between the US and Iran and the direct impact on energy supply and resulting inflation. The base scenario envisages a negotiated reopening of critical shipping routes via the Strait of Hormuz in the coming weeks, while the growing risk of a prolonged delay weighs on this outlook.

Compared to regions with a higher degree of energy self-sufficiency, Europe and parts of emerging Asia are more exposed to the ongoing economic effects of the situation. Growth forecasts have been revised downwards to reflect these pressures, by 0.6 percentage points to 0.8% for the Euro Area (EA), and to 2.8% for the global economy with the continued boom in AI acting as a positive counterbalancing force.

Major central banks are taking notice of the inflationary pressures but have exercised caution in taking actions. The European Central Bank (ECB) left rates unchanged at its April meeting but signalled the possibility of a rate hike in June. Labour markets are less tight than in 2022, and monetary policy starts from broadly neutral conditions. In case of a more significant EA slowdown, a single 25 basis point hike in June may be sufficient, though the market is now pricing three ECB hikes this year.

In the US, the Federal Reserve is expected to look past the price shock, given the growing risks to employment and economic growth.

In this context, for its strategic plan Lifetime Partner 27: Driving Excellence, Generali is focused on executing according to its three strategic priorities, excellence in customer relationships, excellence in core capabilities and excellence in the Group’s operating model and based on its three foundations, People, AI and Data and Sustainability. The Group is deepening its Lifetime Partner relationships with seamless, personalised omni-channel experiences, while accelerating growth in preferred profit pools, increasing technical proficiency and scaling AI and Group-wide assets.

In Life, capitalising on Generali’s broad customer base and strong distribution footprint, Generali’s focus remains on improving technical proficiency and on simplification, offering updated and integrated solutions to adapt to evolving customer needs throughout their lifetime. The main areas of focus include protection and health products, as well as capital-light savings solutions, with the goal of becoming the partner of choice for each customer. The Group’s hybrid and unit-linked offers continue to be a priority to address growing customer needs for financial security with the objective to become the go-to partner for retirement and savings.

In P&C, the Group’s objective is to maximise profitable growth - with a focus on non-motor lines - across the insurance markets where it operates, strengthening its position and offering, especially in countries with high growth potential. The Group confirms and reinforces its flexible approach to tariff adjustments, also considering a general increase in Nat Cat events. The non-motor offer will continue to be enhanced through the addition of modular solutions designed to address specific customer needs. Generali will continue to increase its focus on developing insurance solutions related to the environment and climate change. As part of this, Generali has established the Group Climate Hub, which plays a key role in defining methodologies and approaches to understand and manage physical risks.

With reference to investment policy, the Group will continue to pursue an asset allocation strategy aimed at ensuring consistency with policyholder liabilities and improving risk-adjusted returns with a focus on increasing current income. Investments in private and real assets will continue to be pursued gradually to enhance portfolio diversification and capture opportunities, with a prudent approach that takes into account the lower liquidity and higher complexity of these instruments. In real estate, the Group will pursue a policy of geographical and sectorial diversification, closely monitoring and evaluating market opportunities and asset quality.

In Asset & Wealth Management, Generali will continue to expand its product offering, particularly in real and private assets, and enhance distribution channels while also benefitting from the investment capabilities obtained through the acquisition of MGG Investment Group. In Wealth Management, also thanks to the recent acquisition of Intermonte and the launch of insurbanking, Banca Generali group will focus on enhancing its future growth path and maintaining robust shareholder remuneration.

Through the Lifetime Partner 27: Driving Excellence plan the Group is committed to delivering its ambitious 2025-2027 targets:

- strong earnings per share growth: 8-10% EPS CAGR4;

- solid cash generation: > € 11 billion cumulative Net Holding Cash Flow5;

- Increasing dividend per share6: >10% DPS CAGR7, with ratchet policy

underpinned by a clear capital management framework, with increased focus on shareholder returns:

- over € 7 billion cumulative dividends6 (2025-2027);

- a commitment to a minimum annual € 500 million share buyback, to be assessed at the beginning of each year of the plan (for a total commitment of at least € 1.5 billion6 over the plan), with a € 500 million share buyback executed in 2025 and a further € 500 million to be launched in 20266.

Significant events after 31 March 2026

On April 23th, the 2026 Annual General Meeting approved the 2025 financial statements and dividend distribution, appointed the new Board of Statutory Auditors and approved the € 500 million share buyback6.

On April 27th, Generali announced that the number of shares into which the share capital (fully subscribed and paid up) of Assicurazioni Generali S.p.A. is divided was amended in relation with the cancellation of own shares acquired for the purposes of the share buy-back scheme, approved with resolution of the Shareholders’ General Meeting of April 24th 2025, as part of the implementation of the 2025-27 strategic plan.

On May 4th, Generali was confirmed for the eighth consecutive year in the Dow Jones Best-in-Class World Index and for the seventh consecutive year in the Dow Jones Best-in-Class Europe Index, formerly known as Dow Jones Sustainability Indexes (DJSI).

Other significant events that occurred after the end of the period are available on the website.

***

Q&A conference call

The Direttore Generale – Group Deputy CEO, Giulio Terzariol, the Group CFO, Cristiano Borean and the Group General Manager, Marco Sesana will host the Q&A session conference call for the consolidated results of the Generali Group as of 31 March 2026, which will be held on 21 May 2026 at 12.00 pm CEST.

To follow the conference call, in a listen only mode, please dial +39 02 8020927.

***

The Manager in charge of preparing the company’s financial reports, Cristiano Borean, declares, pursuant to paragraph 2, article 154 bis of the Consolidated Law on Finance, that the accounting information in this press release corresponds to the document results, books and accounting entries.

1Please see the paragraph on adjusted net result on page 3

2 The Financial Information at March 31st 2026 is not an interim Financial Report according to the IAS 34 principle.

3 For definition of the adjusted net result, please refer to page 2.

4 3-year CAGR based on the Group’s adjusted net result.

5 Expressed on cash basis.

6 Subject to all relevant approvals.

7 3-year Dividend per Share (DPS) CAGR with 2024 baseline at € 1.28 per share.